The Code on Wages, 2019 introduced one of the most significant reforms in India’s labour law framework by prescribing a uniform definition of “wages” across multiple labour legislations. While many organisations have focused on restructuring salary components to align with the new definition, an equally important question often remains unanswered:

Are employers interpreting the definition of wages correctly for gratuity, leave encashment, actuarial valuations, and financial reporting?

In discussions with employers, HR professionals, payroll managers, finance teams, actuaries, and statutory auditors, one interpretation frequently emerges:

“As long as Basic Salary, Dearness Allowance (DA), and Retaining Allowance together constitute at least 50% of an employee’s total remuneration, the organisation complies with the Code on Wages.”Although this view is widely accepted, it oversimplifies what the legislation actually provides.

The definition of wages under the Code is far more comprehensive. It begins with all remuneration payable to an employee and then excludes specific components. Even those exclusions are subject to an important condition known as the 50% threshold, under which certain excluded amounts may be added back while computing wages.

For employers, this distinction is not merely a payroll issue. It can significantly affect:

- Gratuity liability

- Leave encashment provisions

- Actuarial valuations

- Employee benefit accounting under AS 15 and Ind AS 19

- Financial statements

- Statutory audits

A misunderstanding of the definition may therefore result in understated employee benefit obligations, incorrect actuarial assumptions, and accounting adjustments during the audit process.

This article examines the definition of wages from a practical perspective and discusses its implications for employers, finance professionals, HR teams, actuaries, and statutory auditors.

Why Was the Definition of Wages Revised?

Before the introduction of the Labour Codes, different labour legislations prescribed different definitions of wages. For example, the Payment of Wages Act, 1936, the Minimum Wages Act, 1948, the Payment of Bonus Act, 1965, and the Equal Remuneration Act, 1976 each adopted their own approach.

This created several practical challenges.

Many organisations structured salaries differently depending on the applicable legislation. Certain salary components were treated as wages under one law but excluded under another, resulting in compliance complexities and inconsistent employee benefit calculations.

To simplify this framework, the Government enacted the Code on Wages, 2019, consolidating four central labour laws into a single legislation with a common definition of wages. The objective was to promote consistency, reduce ambiguity, and discourage artificial salary structuring that could lower statutory employee benefits.

The Ministry of Labour and Employment also introduced the Code on Wages (Central) Rules, 2020, providing operational guidance for implementing the legislation.

Understanding the Definition of Wages under the Code on Wages, 2019

What Does Section 2(y) Actually Provide?

Section 2(y) of the Code on Wages, 2019 defines wages as all remuneration expressed in monetary terms that an employee receives for employment, provided the terms of employment are fulfilled.

Instead of beginning with Basic Salary or Dearness Allowance, the definition starts with total remuneration payable to the employee.

The legislation then specifies certain components that are excluded from wages.

These exclusions include, among others:

- House Rent Allowance (HRA)

- Bonus payable under any law

- Employer’s contribution towards Provident Fund and pension

- Conveyance allowance

- Travelling allowance

- Amounts paid to reimburse special expenses incurred because of employment

- Gratuity payable upon termination of employment

- Certain retrenchment compensation and terminal benefits

However, the definition does not end there.

The Code introduces an important safeguard.

If the aggregate value of these excluded components exceeds 50% of the employee’s total remuneration, the amount exceeding that limit is added back while computing wages.

This means the law begins with total remuneration—not merely Basic Salary plus Dearness Allowance and then adjusts the computation based on the statutory exclusions and the prescribed threshold.

Understanding this sequence is essential because many payroll interpretations begin with Basic Salary and attempt to satisfy the 50% rule, whereas the legislation follows the reverse approach.

Understanding the 50% Rule

The 50% threshold is perhaps the most discussed aspect of the revised definition of wages.

However, it is also one of the most misunderstood.

Many organisations interpret the provision as requiring Basic Salary, Dearness Allowance, and Retaining Allowance to account for at least half of an employee’s salary package.

The legislation does not use this methodology.

Instead, the Code first considers the employee’s total remuneration.

It then excludes only those components specifically identified under Section 2(y).

If the total value of these exclusions exceeds 50% of total remuneration, the excess amount is brought back into wages.

The legislative intent behind this provision is equally important.

Over the years, salary structures increasingly relied on multiple allowances while keeping Basic Salary relatively low. Since several statutory benefits are linked to wages, such structures often reduced employer liabilities for gratuity and other benefits.

By introducing the 50% threshold, the legislature sought to ensure that statutory employee benefits are determined on a more representative portion of an employee’s remuneration rather than being significantly diluted through salary structuring.

Consequently, compliance requires more than checking whether Basic Salary constitutes half of the salary package. Employers must evaluate the nature of each salary component, determine whether it qualifies for exclusion under the Code, and assess whether the aggregate exclusions exceed the statutory limit.

Why the Nature of Salary Components Matters?

One of the most important principles emerging from the revised definition is that the substance of a payment is generally more important than its label.

Merely describing a salary component as “Special Allowance,” “Performance Bonus,” or “Incentive” does not automatically determine whether it should be included in or excluded from wages.

Each component should be evaluated based on:

- Its contractual terms.

- The purpose of the payment.

- Whether it falls within a specific statutory exclusion under Section 2(y).

- Whether the exclusion remains within the 50% threshold.

This principle requires employers and auditors to move beyond payroll nomenclature and examine the actual character of each payment while determining wages.

Practical Salary Illustration: How to Calculate Wages Under the Code on Wages

Understanding the statutory definition becomes much easier when we apply it to a practical salary structure. More importantly, this exercise demonstrates why organisations should evaluate the substance of each salary component rather than relying solely on its name.

Consider the following monthly salary structure.

| Salary Component | Amount (₹) |

|---|---|

| Basic Salary | 1,17,500 |

| House Rent Allowance (HRA) | 47,000 |

| Performance Bonus | 20,000 |

| Special Allowance | 15,000 |

| Leave Travel Allowance (LTA) | 8,000 |

| Incentive | 27,500 |

| Total Monthly Remuneration | 2,35,000 |

At first glance, many payroll teams conclude that since the Basic Salary is approximately 50% of the total remuneration, the organisation complies with the Code on Wages. However, that is not how Section 2(y) operates.

The correct approach is to begin with the employee’s total remuneration and then examine each component individually to determine whether it qualifies for exclusion under the Code. Only after identifying the eligible exclusions should the employer assess whether the aggregate exclusions exceed the statutory 50% threshold.

This component-by-component analysis is particularly important because two salary components with similar names may receive different treatment depending on their contractual nature and purpose.

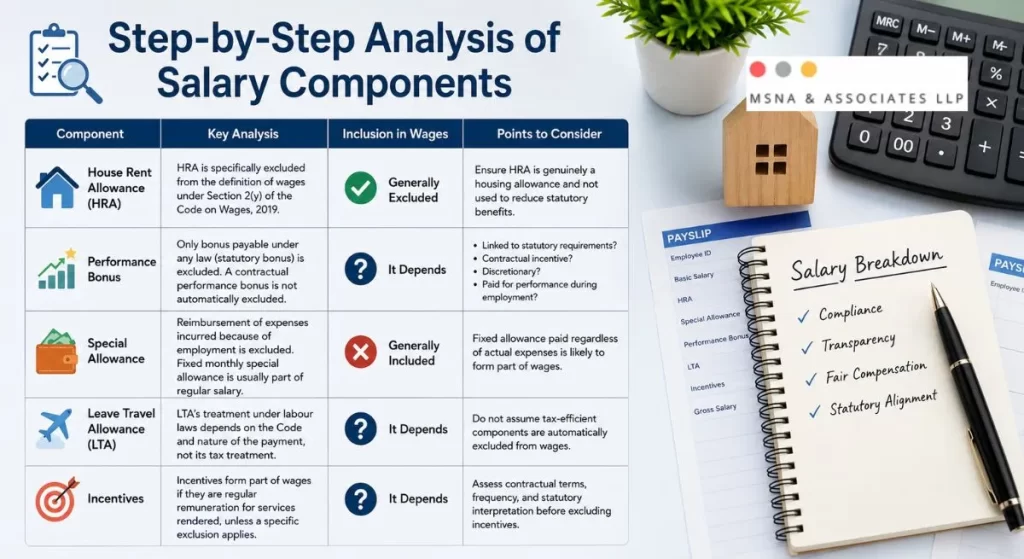

Step-by-Step Analysis of Salary Components

1. House Rent Allowance (HRA)

House Rent Allowance is specifically excluded from the definition of wages under Section 2(y) of the Code on Wages, 2019. Therefore, employers can generally exclude HRA while computing wages.

2. Performance Bonus:

Performance Bonus often creates uncertainty because many payroll systems classify every payment described as a “bonus” as an excluded component.

The Code, however, excludes bonus payable under any law, such as a statutory bonus payable under the applicable labour legislation. A contractual performance bonus does not automatically qualify for exclusion merely because it contains the word “bonus.”

Employers should therefore examine:

- Is the payment linked to statutory requirements?

- Is it a contractual incentive?

- Is it discretionary?

- Is it paid for performance achieved during employment?

The legal character of the payment is more important than the terminology used in the salary structure.

From an audit perspective, organisations should maintain documentation supporting the basis for treating a performance bonus as either included in or excluded from wages.

3. Special Allowance

Among all salary components, Special Allowance is perhaps the most frequently misunderstood.

Many organisations assume that Special Allowance falls within the statutory exclusion relating to “special expenses incurred because of employment.” Consequently, they exclude it while calculating wages.

This interpretation deserves careful consideration.

The Code excludes amounts paid to reimburse expenses incurred because of employment. Examples may include reimbursements for official travel, client visits, or other employment-related expenses supported by bills or company policy.

A fixed monthly Special Allowance, however, generally forms part of the employee’s regular salary package. It is paid irrespective of whether the employee incurs any specific employment-related expenditure and therefore differs fundamentally from a reimbursement.

Accordingly, where a Special Allowance represents fixed remuneration rather than reimbursement of expenses, it may continue to form part of wages, subject to the specific facts and contractual terms.

This distinction illustrates an important compliance principle: payroll nomenclature does not determine legal treatment. Employers should evaluate the underlying purpose and character of the payment before deciding whether it qualifies for exclusion.

4. Leave Travel Allowance (LTA)

Leave Travel Allowance is another component that requires careful evaluation.

Although LTA is commonly treated as a tax-efficient salary component under the Income-tax Act, its treatment under labour legislation depends on the wording of the Code and the nature of the payment.

Employers should avoid assuming that a component’s tax treatment automatically determines its treatment under labour laws. Tax legislation and labour legislation operate independently and serve different objectives.

A comprehensive review of salary components should therefore distinguish between tax planning considerations and statutory employee benefit obligations.

5. Incentives

Sales incentives, productivity incentives, and performance-linked incentives are increasingly common across industries.

Whether such payments form part of wages depends on their contractual terms, frequency, and statutory interpretation.

If an incentive forms part of the employee’s regular remuneration for services rendered, employers should carefully assess whether any statutory exclusion actually applies before excluding it from wages.

A blanket policy of excluding all incentives may not always reflect the intent of the legislation.

Illustrative Computation of Wages

Based on the above salary structure and assuming that only House Rent Allowance qualifies for exclusion while the remaining components continue to form part of wages, the computation would appear as follows:

| Particulars | Amount (₹) |

|---|---|

| Total Monthly Remuneration | 2,35,000 |

| Less: House Rent Allowance | (47,000) |

| Illustrative Wages | 1,88,000 |

Illustrative Note: This example is intended for educational purposes. The actual computation depends on the contractual terms, the true nature of each salary component, and the application of the statutory exclusions under Section 2(y) of the Code on Wages, 2019.

Common Payroll Mistakes Employers Should Avoid

During payroll reviews and discussions with management, certain recurring issues frequently emerge.

1. Assuming Basic Salary Alone Determines Compliance

Many organisations focus exclusively on ensuring that Basic Salary constitutes at least 50% of the salary package.

This approach overlooks the statutory methodology prescribed under the Code, which begins with total remuneration rather than Basic Salary.

2. Treating Every Allowance as an Excluded Component

Another common mistake is assuming that all allowances automatically fall outside the definition of wages.

The Code specifies only certain exclusions. Employers should evaluate each allowance individually instead of applying a blanket approach.

3. Ignoring the Substance of Payments

Payroll descriptions such as “Special Allowance,” “Retention Allowance,” “Performance Incentive,” or “Flexi Benefit” do not determine legal treatment.

The actual purpose of the payment remains the decisive factor.

This principle is consistent with broader judicial reasoning in employment law, where courts often examine the real substance of remuneration rather than its nomenclature.

4. Relying Solely on Payroll Software

Many payroll systems calculate statutory benefits based on predefined salary heads.

While automation improves efficiency, payroll software cannot substitute for legal interpretation. Organisations should periodically review salary structures with their HR, finance, legal, and tax advisors to ensure continued compliance with evolving labour laws.

Practical Implications for Employers

The revised definition of wages should not be viewed merely as a payroll compliance requirement.

It has implications across multiple business functions.

- Human Resources should review appointment letters, compensation structures, and employee benefit policies.

- Payroll Teams should evaluate whether salary components have been correctly classified and whether payroll systems accurately reflect the statutory definition.

- Finance Teams should assess the impact on gratuity, leave encashment, actuarial valuations, and financial reporting.

- Management should understand that changes in wage computation may increase employee benefit obligations and should plan accordingly.

A coordinated review involving HR, payroll, finance, actuaries, and legal advisors can help organisations avoid compliance gaps and ensure that employee benefit liabilities are recognised appropriately

Why the Definition of Wages Matters for Gratuity, Leave Encashment and Employee Benefit Accounting?

Understanding the definition of wages under the Code on Wages is not merely a payroll compliance exercise. It has significant implications for employee benefit obligations, actuarial valuations, financial reporting, and statutory audits.

Many organisations initially viewed the revised definition as a change in salary structuring. In reality, it has the potential to increase long-term employee benefit liabilities, particularly where gratuity and leave encashment are linked to wages.

The impact becomes even more significant for organisations with a large workforce. A relatively small increase in the salary considered for employee benefits can translate into a substantial increase in actuarial liabilities when multiplied across hundreds or thousands of employees.

How the Revised Definition Can Increase Gratuity Liability?

Gratuity is one of the most significant long-term employee benefits provided under the Payment of Gratuity Act, 1972. Traditionally, many organisations calculated gratuity based only on Basic Salary and Dearness Allowance (DA) because these components generally constituted wages for gratuity purposes.

However, if an employer restructures salary components to comply with the revised definition of wages under the Code on Wages, the salary considered for gratuity may increase.

Consider the earlier illustration.

| Particulars | Earlier Practice | Revised Illustration |

|---|---|---|

| Salary considered for gratuity | ₹1,17,500 | ₹1,88,000 |

| Increase | ₹70,500 |

The increase of ₹70,500 relates to just one employee.

Now consider an organisation employing:

- 250 employees

- 1,000 employees

- 5,000 employees

Even if only a portion of the workforce experiences a similar increase in wages for gratuity purposes, the cumulative actuarial liability could increase significantly.

For employers, this highlights an important business consideration. Salary restructuring should not be viewed in isolation from employee benefit costs. A change in wage composition may improve compliance with labour laws while simultaneously increasing gratuity obligations that must be recognised in the financial statements.

Impact on Leave Encashment Provisions

Gratuity is not the only employee benefit affected by the revised wage definition.

Many organisations also calculate leave encashment based on salary components linked to wages. If the salary base increases because of the revised wage definition, leave encashment obligations may also increase.

Unlike short-term payroll expenses, leave encashment is generally recognised as a long-term employee benefit under AS 15 or Ind AS 19, depending on the applicable financial reporting framework.

The Institute of Chartered Accountants of India (ICAI) has also observed that the revised definition of wages under the Labour Codes may increase leave obligations. Where the change results in higher employee benefits, the corresponding impact should be recognised in accordance with the applicable accounting standards.

For finance teams, this means that the effect extends beyond payroll processing. It directly influences:

- Employee benefit provisions

- Profit and Loss Account

- Balance Sheet liabilities

- Actuarial valuation reports

- Financial statement disclosures

Organisations that revise gratuity calculations should therefore evaluate leave encashment provisions simultaneously rather than treating both benefits independently.

The Accounting Perspective: Why This Is More Than an Actuarial Change

This is where the discussion moves beyond labour law and enters the realm of financial reporting.

Many organisations assume that if gratuity liability increases because of the revised wage definition, the increase should simply be reflected through the actuarial valuation as part of the annual remeasurement exercise.

However, the accounting treatment requires a more careful analysis.

The ICAI’s Educational Material on Ind AS 19 and AS 15 explains that where employee benefits increase because the benefit formula itself has changed, the increase may not merely represent an actuarial assumption change. Instead, it may constitute a plan amendment, depending on the facts and circumstances.

This distinction is critical because plan amendments and actuarial gains or losses are recognised differently under the applicable accounting standards.

Understanding Plan Amendments and Past Service Cost

To understand why the accounting treatment changes, consider the following example.

Assume an employee has already completed 12 years of continuous service.

Until now, gratuity has been calculated on a wage base of ₹1,17,500.

Following the implementation of the revised wage definition, the gratuity salary increases to ₹1,88,000, without any corresponding increase in the employee’s overall remuneration.

The question is straightforward:

Does the additional gratuity liability relate only to future service?

The answer is no.

The employee has already rendered twelve years of service under the gratuity plan. Once the wage definition used for calculating gratuity changes, the enhanced benefit also applies to those years already served.

Accordingly, the increase is not confined to future employment. It also relates to services rendered in previous years.

This is precisely why accounting standards classify such an increase as Past Service Cost when it arises because of a plan amendment.

In simple terms:

- Future service creates the current service cost recognised each year.

- Changes in actuarial assumptions, such as salary escalation or discount rates, result in actuarial gains or losses.

- Changes in the benefit formula, such as a revised wage definition that enhances employee benefits, may result in Past Service Cost.

Understanding this distinction is essential for finance teams because it determines how the increased liability is recognised in the financial statements.

What Happens When Salary Is Restructured Without Increasing Overall Remuneration?

One practical situation frequently encountered by employers involves restructuring salary components solely to align with the revised definition of wages.

For example, an organisation may increase Basic Salary while proportionately reducing allowances, leaving the employee’s total cost to company (CTC) unchanged.

Many employers assume that because there is no increase in total salary, there should be no additional accounting implications.

However, this assumption may not always be correct.

If the restructuring increases the wage base used for gratuity or leave encashment, the employee’s benefit entitlement may increase even though the overall remuneration remains unchanged.

The ICAI has clarified that where salary restructuring effectively enhances employee benefits under the existing gratuity plan, the resulting increase in liability should generally be evaluated as a plan amendment, giving rise to Past Service Cost.

This illustrates an important point:

The accounting impact depends on the change in employee benefits—not merely on whether total salary has increased.

What If the Organisation Also Grants an Annual Salary Increment?

In practice, organisations often revise salary structures during the annual appraisal cycle.

Suppose an employee receives:

- a regular annual salary increment; and

- a revised salary structure to comply with the Code on Wages.

In such cases, the increase in gratuity liability may arise from two different factors.

The first relates to the normal annual increase in salary.

The second arises because the revised wage definition changes the basis on which employee benefits are calculated.

The accounting implications should therefore be analysed separately.

Conceptually, the overall increase may need to be attributed between:

- the increase resulting from normal salary escalation; and

- the increase arising from the revised benefit formula or plan amendment.

Separating these effects helps ensure that the accounting treatment appropriately reflects the underlying economic event.

Why This Matters for Financial Reporting?

Employee benefit obligations are often among the most significant long-term liabilities recognised in an organisation’s financial statements.

An incorrect interpretation of the wage definition can therefore have consequences that extend beyond payroll compliance.

Potential implications include:

- Understatement of gratuity liability.

- Understatement of leave encashment provisions.

- Incorrect actuarial valuation assumptions.

- Misclassification of employee benefit expenses.

- Inadequate disclosures in financial statements.

- Audit qualifications or management observations where the impact is material.

For organisations reporting under Ind AS, employee benefit accounting is particularly important because investors, lenders, regulators, and other stakeholders rely on the accuracy of long-term liability disclosures.

Accordingly, management should ensure that payroll practices, actuarial assumptions, and accounting treatments are aligned and supported by appropriate documentation.

One of the most common observations during discussions with employers is that payroll, HR, finance, and actuarial teams often evaluate the revised wage definition independently. Payroll focuses on salary restructuring, HR reviews compensation policies, actuaries update valuation assumptions, and finance records the accounting impact. However, these activities are closely interconnected. A coordinated review across all functions is far more likely to identify compliance issues early and ensure that employee benefit obligations are measured and reported consistently.

What Should Statutory Auditors Verify?

For statutory auditors, obtaining an actuarial valuation report should be the starting point rather than the conclusion of the audit process.

The revised definition of wages under the Code on Wages may significantly influence gratuity and leave encashment liabilities. Consequently, auditors should assess not only the actuarial assumptions but also whether management has correctly interpreted the underlying legal provisions.

The audit objective is not to question the actuary’s expertise but to evaluate whether the actuarial valuation is based on appropriate inputs and whether the resulting accounting treatment complies with the applicable financial reporting framework.

1. Review Management’s Interpretation of Wages

Auditors should first understand how management has interpreted the revised definition of wages.

Some useful questions include:

- Has management formally documented its interpretation of Section 2(y) of the Code on Wages, 2019?

- Have all salary components been analysed individually?

- Has the organisation evaluated whether each exclusion specifically falls within the statutory definition?

- Is the interpretation consistently applied across all employee categories?

A documented assessment demonstrates that management has exercised due diligence rather than relying solely on payroll conventions.

2. Evaluate the Salary Structure

The salary structure often provides the first indication of whether employee benefit obligations may have changed.

Auditors should review:

- Basic Salary

- Dearness Allowance

- Retaining Allowance

- House Rent Allowance

- Special Allowance

- Performance Bonus

- Incentives

- Leave Travel Allowance

- Employer’s PF contribution

- Other recurring allowances

Merely reviewing payroll software reports may not be sufficient. The contractual terms governing each salary component should also be examined.

3. Review the Actuarial Valuation

The actuarial report should be read in conjunction with the employer’s compensation policy.

Auditors should consider whether:

- the actuary has incorporated the revised wage definition;

- the salary used for gratuity reflects management’s approved wage structure;

- assumptions regarding future salary growth remain reasonable;

- the valuation methodology is consistent with the applicable accounting standards; and

- the report adequately explains any significant increase in employee benefit obligations.

Where the revised wage definition has materially affected the valuation, auditors should understand how the actuary has incorporated the impact.

4. Assess the Accounting Treatment

An increase in employee benefit liability does not automatically imply that the entire increase represents an actuarial gain or loss.

Auditors should evaluate whether management has appropriately analysed:

- current service cost;

- interest cost;

- actuarial gains or losses;

- plan amendments;

- Past Service Cost; and

- financial statement disclosures.

This assessment becomes particularly important where the employer has restructured salary components to comply with the revised wage definition.

4. Review Leave Encashment Valuation

Many organisations focus exclusively on gratuity while overlooking leave encashment.

Where leave encashment is linked to wages or salary components affected by the revised definition, auditors should determine whether the corresponding actuarial valuation has also been updated.

Ignoring leave encashment may result in incomplete recognition of employee benefit obligations.

Employer Compliance Checklist

Before implementing or reviewing salary restructuring, employers should consider the following checklist.

| Review Area | Questions to Consider |

|---|---|

| Salary Structure | Have all salary components been reviewed individually? |

| Wage Definition | Does the computation begin with total remuneration as required by Section 2(y)? |

| 50% Threshold | Have statutory exclusions been evaluated before applying the threshold? |

| Payroll Policy | Are payroll practices consistent across employee categories? |

| Gratuity | Has the gratuity valuation been revisited? |

| Leave Encashment | Has the leave liability also been reassessed? |

| Actuarial Valuation | Has the actuary been informed of revised wage assumptions? |

| Accounting | Has the accounting treatment been evaluated under AS 15 or Ind AS 19? |

| Documentation | Has management documented its interpretation of the revised wage definition? |

| Audit Readiness | Are supporting documents available for audit review? |

A structured review helps organisations identify compliance issues before they affect financial reporting or statutory audits.

Common Misconceptions About the Definition of Wages

Several misconceptions continue to circulate despite the revised legislative framework.

1.”Basic Salary Must Simply Be 50%”

This is perhaps the most common misunderstanding.

The Code does not merely require employers to increase Basic Salary until it reaches 50% of total remuneration.

Instead, the legislation prescribes a sequence:

- Begin with total remuneration.

- Identify the statutory exclusions.

- Evaluate whether the exclusions exceed 50%.

- Add back the excess while computing wages.

Understanding this sequence is essential for correct compliance.

2. “Every Allowance Is Automatically Excluded”

The Code specifically lists the components that may be excluded.

An allowance should not be excluded solely because it is described as an allowance in the payroll system.

Its legal character and contractual purpose should always be examined.

3. The Change Only Affects Payroll

This assumption overlooks the broader financial implications.

Changes in the wage definition may affect:

- gratuity;

- leave encashment;

- actuarial liabilities;

- financial statements;

- audit procedures; and

- employee benefit disclosures.

Accordingly, organisations should adopt a cross-functional approach involving HR, payroll, finance, legal, and actuarial teams.

Key Takeaways

The revised definition of wages under the Code on Wages represents far more than a change in payroll terminology. It introduces a structured framework for determining wages that may influence employee benefit liabilities, actuarial valuations, and financial reporting.

For employers, compliance should not be limited to ensuring that Basic Salary constitutes a specified proportion of the salary package. The correct approach requires evaluating the nature of each salary component, applying the statutory exclusions prescribed under Section 2(y), and assessing the operation of the 50% threshold.

For finance professionals, the revised definition may have implications for gratuity, leave encashment, and employee benefit accounting under AS 15 and Ind AS 19.

For statutory auditors, reviewing actuarial reports without understanding the underlying wage assumptions may leave important audit risks unidentified. Audit procedures should therefore extend beyond numerical accuracy to include management’s interpretation of the applicable legal provisions and the consistency of the accounting treatment.

Ultimately, the revised definition reinforces a principle that applies across accounting, auditing, and labour law:

Compliance depends not only on the numbers reported but also on whether the underlying principles have been correctly understood and consistently applied.

Need to Evaluate the Impact of the Revised Wage Definition?

Related

Discover more from MSNA & Associates LLP

Subscribe to get the latest posts sent to your email.