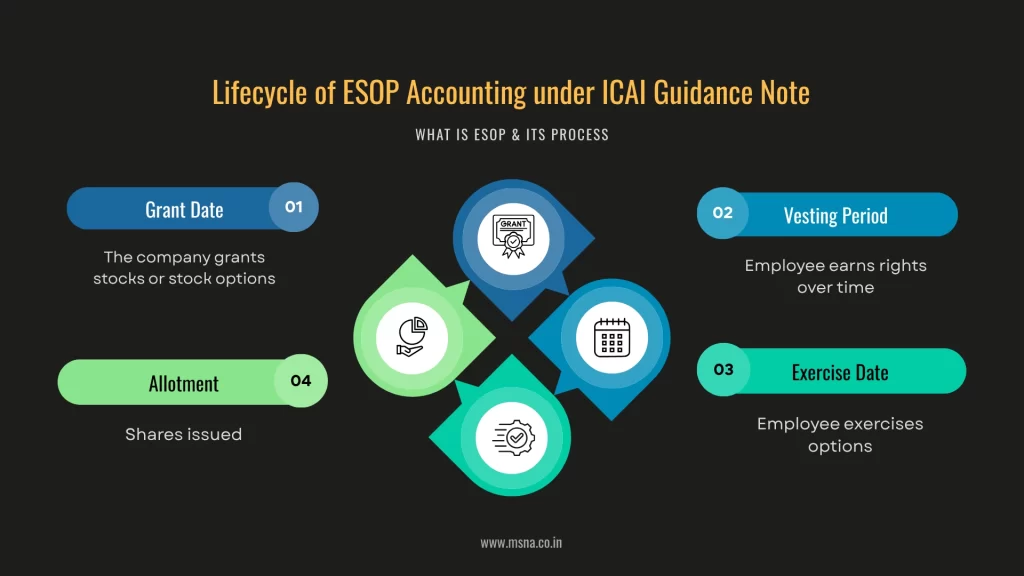

Accounting for ESOPs as per ICAI Guidance Note: A Quick Note

Companies that follow Accounting Standards under the Companies (Accounting Standards) Rules, 2006, account for Employee Stock Option Plans by recognizing employee compensation cost over the vesting period. They usually measure this cost through either the fair value method or the intrinsic value method, depending on the policy they adopt and the requirements of the Guidance Note.

In simple terms, the company recognizes the value of employee services received in exchange for ESOPs. For equity-settled ESOPs, it credits equity, generally through an ESOP reserve. For cash-settled arrangements, it recognizes a liability and remeasures that liability until settlement.

Who Should Read This ESOP Accounting Guide?

- Finance teams who are preparing financial statements under the Indian Accounting Standards framework applicable to AS-compliant companies.

- Chartered accountants and auditors reviewing ESOP expense, vesting schedules, and disclosures.

- Startup founders and CFOs who want to understand how ESOP grants affect profit and loss, equity, and reporting.

- The company secretarial and compliance teams those are coordinating ESOP documentation with accounting treatment.

Overview of Employee Stock Option Plans (ESOPs)

In many countries, shares and share options comprise a significant element of the total remuneration package of senior personnel; a trend encouraged by the current consensus that, it is a matter of good corporate governance to promote significant long-term shareholdings by senior management, so as to align their economic interests with those of shareholders.

The plans include Employee Stock Option Plans (ESOPs), Employee Stock Purchase Plans (ESPPs) and Stock Appreciation Rights (SARs).

ESOPs are plans under which an enterprise grants options for a specified period to its employees to purchase its shares at a fixed or determinable price.

Applicability of ICAI Guidance Note for ESOP Accounting

This Guidance Note applies exclusively to companies that follow Accounting Standards (AS) under the Companies (Accounting Standards) Rules, 2006, and does not apply to entities that report under Ind AS, companies governed by the Companies (Indian Accounting Standards) Rules, 2015.

Scope of Share-Based Payment Transactions Covered

This Guidance Note establishes financial accounting and reporting principles for share-based payment plans, including ESOPs, ESPPs, and SARs, as well as share-based payment arrangements with non-employees.

The Guidance Note must be applied to all share-based payment transactions, including:

- equity-settled share-based payment transactions;

- cash-settled share-based payment transactions; and

- transactions where either the enterprise or the supplier of goods or services can choose whether the transaction is to be equity- settled or cash-settled.

This article deals only with the accounting of ESOPs as per the guidance note and does not cover all other share-based payments.

What This Entire Article Covers About ESOPs?

This guide focuses on accounting treatment for ESOPs under the ICAI Guidance Note. It explains when a company recognises ESOP cost, how it measures options, how vesting affects expense recognition, and what the company should disclose in its financial statements.

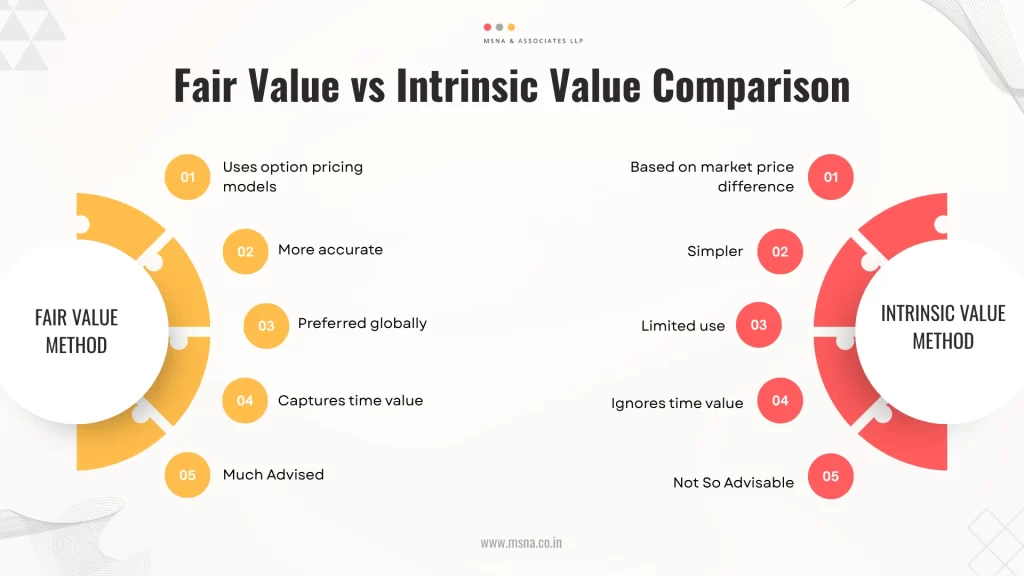

ESOP Accounting Methods: Fair Value Method and Intrinsic Value Method

|

Method |

What it Measures |

How it Affects Accounting |

|

Fair Value Method |

It measures the fair value of the equity instruments granted, usually at the grant date. |

The company recognises employee compensation cost over the vesting period based on the fair value determined. |

|

Intrinsic Value Method |

It measures the excess of the market value of the underlying share over the exercise price. |

The company uses intrinsic value in place of fair value and remeasures it where the Guidance Note requires such treatment. |

For stronger financial reporting, many companies prefer a fair value-based approach because it captures the economic value of options more comprehensively than a pure intrinsic value approach.

What is the Fair Value Method for ESOP Accounting?

Here’s the technical definition of the fair value method – the enterprise shall measure the goods or services received, and the corresponding increase in equity, directly, at the fair value of the goods or services received, unless that fair value cannot be estimated reliably.

If the enterprise cannot estimate reliably the fair value of the goods or services received, the enterprise shall measure their value, and the corresponding increase in equity, indirectly, by reference to the fair value of the equity instruments granted.

With respect to ESOPs, the enterprise shall measure the fair value of the services received by reference to the fair value of the equity instruments granted, because typically it is not possible to estimate reliably the fair value of the services received. The fair value of those equity instruments that vest immediately without any requirement of a vesting period shall be measured at the grant date.

If the equity instruments granted do not vest until the counterparty completes a specified period of service, the enterprise should presume that the services to be rendered by the counterparty as consideration for those instruments will be received in the future, during the vesting period. The enterprise should account for those services as they are rendered by the employee during the vesting period, on a time proportion basis, with a corresponding credit to the equity account.

What is the Intrinsic Value Method for ESOP Accounting?

Intrinsic value is the amount by which the fair value (the quoted market price) of the underlying share exceeds the exercise price of an option.

For example, an option with an exercise price of Rs. 100 on an equity share whose current quoted market price is Rs. 125 has an intrinsic value of Rs. 25 per share on the date of its valuation. In the case of a non-listed company, since shares are not quoted on a stock exchange, the value of its shares is determined based on the valuation report from an independent valuer.

For accounting of share-based payment plans, the intrinsic value may be used, with the necessary changes having been made in place of the fair value as described in the paragraphs above.

Example of an Intrinsic Value of an ESOP

Assume an employee of yours receives an option with an exercise price of Rs.100, while the market price of the share is Rs. 125 on the relevant measurement date. The intrinsic value equals Rs. 25 per option. If the option is out of the money, the intrinsic value may be nil even though the option can still have time value.

How to Determine the Fair Value of ESOPs?

The fair value of the equity instruments shall always be measured at the grant date. The method of determination of fair value depends on the type of instruments issued, shares or share options.

Fair Value of ESOPs Based on Shares

The fair value of the shares granted should be measured at the market price of the shares of the enterprise (or an estimated value based on the valuation report of an independent valuer, if the shares of the enterprise are not publicly traded), then it must be adjusted to take into account the terms and conditions upon which the shares were granted.

Fair Value of ESOPs Based on Share Options

For share options granted to employees, in many cases, market prices are not available because the options granted are subject to terms and conditions that do not apply to traded options. When market prices of options are not available, companies are required to apply an option pricing model.

To calculate the fair value of ESOPs, Black Scholes Merton formula & Binomial Model are the two common models used.

How Do We Perform Remeasurement of ESOPs Under Fair Value and Intrinsic Value Methods?

Under the fair value method for equity-settled share-based payment transactions, the fair value of the equity instruments granted is measured at the grant date and, once determined, is not subsequently remeasured. After recognizing employee services over the vesting period, the enterprise shall make no subsequent adjustment to total equity after the vesting date, and changes in the market price of shares do not affect the amount recognized; only revisions in the number of equity instruments expected to vest due to non-market vesting conditions are adjusted during the vesting period.

Where the intrinsic value method is applied, the equity instruments are measured at their intrinsic value initially and remeasured at the end of each reporting period and at the date of final settlement, with changes in intrinsic value recognized in profit or loss.

Practical Example: ESOP Expense Recognition Over Vesting Period

Assume a company grants 10,000 options to employees. The fair value per option at the grant date is Rs.30, and the options vest over three years. The total employee compensation cost equals Rs. 3,00,000. If the company expects the employees to complete the vesting period, it recognizes Rs.1,00,000 each year over three years, subject to the Guidance Note and any changes in expected vesting.

|

Year |

Expense Recognized |

Accounting Logic |

|

Year 1 |

Rs.1,00,000 |

The company recognizes one-third of the total expected employee compensation cost. |

|

Year 2 |

Rs.1,00,000 |

The company continues to recognize the cost as employees render services. |

|

Year 3 |

Rs.1,00,000 |

The company completes recognition when the vesting period ends. |

How To Recognize ESOP Expense in Financial Reporting?

Recognition under the Guidance Note is centered around the principle that the cost of employee services received in exchange for share-based payments, that must be reflected in the company’s financial statements

When to Recognise?

- The company should recognize employee services as they are rendered.

- If the options vest immediately, it is presumed that services have already been received, and the full cost is recognized on the grant date.

- If the options vest over a period of time, the cost is recognized over the vesting period on a straight-line or time-proportion basis.

What to Recognise?

- For equity-settled transactions, the recognition is made as an increase in equity.

- For cash-settled transactions, the recognition is made as a liability, which is remeasured at fair value until settlement.

How To Treat ESOPs After Vesting Date?

Once the options have vested, the enterprise shall make no subsequent adjustment to the total amount recognised in equity for the services received. Accordingly –

- If vested options lapse unexercised, or

- If vested options are forfeited after vesting,

The amount already recognised is not reversed. However, transfers within equity (for example, from an ESOP reserve to a general reserve) are permitted. This principle reflects the fact that the employee services have already been received by the enterprise.

Accounting for ESOP Modifications, Cancellations and Settlements

Enterprises may modify the terms and conditions of ESOPs after the grant date. Common examples include repricing of options, changes in vesting conditions, or settlement of options before vesting.

How to Do Accounting for Modifications?

Where modifications increase the fair value of the options or are otherwise beneficial to the employee, the enterprise shall recognise, in addition to the grant date fair value, the incremental fair value arising from the modification.

The incremental fair value is measured as the difference between-

- the fair value of the modified options, and

- the fair value of the original options,

- measured at the date of modification.

This incremental amount is recognised over the remaining vesting period, in addition to the original expense.

Cancellations and Settlements During Vesting Period:

If an ESOP is cancelled or settled during the vesting period (other than due to failure to satisfy vesting conditions), the enterprise shall account for such cancellation or settlement as an acceleration of vesting. The entire unrecognised expense relating to the options is recognised immediately.

Any payment made to the employee on cancellation or settlement is treated as a deduction from equity, except to the extent that it exceeds the fair value of the options at the cancellation date, in which case the excess is recognised as an expense.

If replacement options are granted and identified as replacement awards, the transaction is accounted for as a modification of the original grant.

What is Graded Vesting of Employee Stock Options?

In many Employee Stock Option Plans, the options granted do not vest on a single date. Instead, vesting occurs in tranches over multiple periods, commonly referred to as graded vesting.

The concept of Graded Vesting – Under a graded vesting schedule, different portions of the options granted vest at different points in time, subject to the satisfaction of vesting conditions. Although the options are granted under a single ESOP scheme, each tranche has:

- a different vesting date,

- a different vesting period, and

- potentially a different expected life

How to Treat Graded Vesting of ESOP in Accounting?

The Guidance Note requires that, in the case of graded vesting, the total ESOP grant be segregated into separate groups, based on the respective vesting dates. Each tranche is treated as a separate grant for the purpose of accounting. Accordingly –

- Each tranche is measured independently at the grant date based on its own vesting period and expected life.

- The fair value of each tranche is recognised as employee compensation cost over its respective vesting period on a time-proportion basis.

- The total ESOP expense recognised in the financial statements represents the aggregate expense of all tranches for the reporting period.

This approach ensures that the pattern of expense recognition appropriately reflects the pattern in which employee services are received.

Common Mistakes To Avoid in ESOP Accounting

Treating the entire ESOP cost as an expense only when employees exercise the options.

- Ignoring expected forfeitures while estimating the employee compensation cost during the vesting period.

- Using one vesting period for a graded vesting plan even when each tranche vests on a different date.

- Reversing amounts already recognized for vested options that lapse unexercised.

- Missing disclosures on valuation assumptions, option movement and the effect of ESOPs on profit and equity.

What Disclosures Are Required for ESOPs?

Disclosures form a critical component of accounting for ESOPs under the Guidance Note. The disclosure requirements are designed to enable users of financial statements to understand:

- The nature and extent of share-based payment arrangements,

- How the fair value of options or shares was determined, and

- The effect of such arrangements on the financial performance and financial position of the enterprise.

Disclosure of the Nature and Extent of ESOPs:

An enterprise is required to disclose a description of each type of employee share-based payment plan that existed during the reporting period, including:

- Vesting requirements,

- Maximum contractual life of options, and

- Method of settlement (equity-settled or cash-settled).

Where plans are substantially similar, disclosures may be aggregated, provided such aggregation does not impair understanding.

ESOP Disclosure Checklist for Accounting Companies & Finance Heads –

- Describe each ESOP plan that existed during the reporting period.

- Explain vesting conditions, contractual life and settlement method.

- Present movement in options, including granted, vested, exercised, forfeited, lapsed and outstanding options.

- Disclose the valuation method and key assumptions used in the option pricing model.

- Explain the effect of ESOP expense on profit or loss and the related impact on equity or liabilities.

- State the accounting policy for ESOPs clearly in the notes to financial statements.

Conclusion

ESOP accounting requires more than a mechanical calculation. A company must identify the applicable framework, measure the options properly, recognise employee compensation cost over the correct vesting period and present transparent disclosures.

When finance teams document assumptions, valuation methods and option movements clearly, they improve audit readiness and help stakeholders understand the true cost of employee share-based compensation. If you want our team at MSNA to assist in drafting ESOP scheme, get in touch with our Virtual CFO team in Bangalore can help you.

Related

Discover more from MSNA & Associates LLP

Subscribe to get the latest posts sent to your email.