PMS Pool Trading Process in India: How Trades Move from Trade Sheet to Client Settlement

Portfolio Management Services (PMS) provide professional investment management to high-net-worth investors in India. While investors often focus on portfolio performance, very few understand how trades actually move from the portfolio manager’s decision to final settlement in their Demat account.

Behind every PMS transaction lies a structured and regulated workflow. Portfolio managers often execute trades at the pooled level and later allocate them to individual client portfolios in accordance with regulatory guidelines.

This mechanism, known as the PMS pool trading process in India, improves operational efficiency while maintaining strict compliance with capital market regulations.

In this article, we explain how PMS pool trading works, the regulatory framework governing it, and how different market participants ensure transparent trade allocation and settlement.

What is the PMS Pool Trading Process in India?

The PMS pool trading process in India refers to the operational mechanism through which a portfolio manager aggregates buy or sell orders across multiple client portfolios and executes them as a single order on the stock exchange.

After execution, the portfolio manager allocates the executed trades across client portfolios on a pro-rata basis using the weighted average price of the day’s trades.

This structure allows PMS providers to:

execute trades more efficiently

maintain price uniformity across portfolios

reduce operational complexity

streamline settlement through custodians

However, regulators require strict safeguards to ensure fairness.

According to the Securities and Exchange Board of India, portfolio managers must ensure transparent allocation and cannot retain open positions during the allocation process.

Additionally, SEBI mandates a minimum investment of ₹50 lakh for PMS accounts in India under the SEBI (Portfolio Managers) Regulations, 2020.

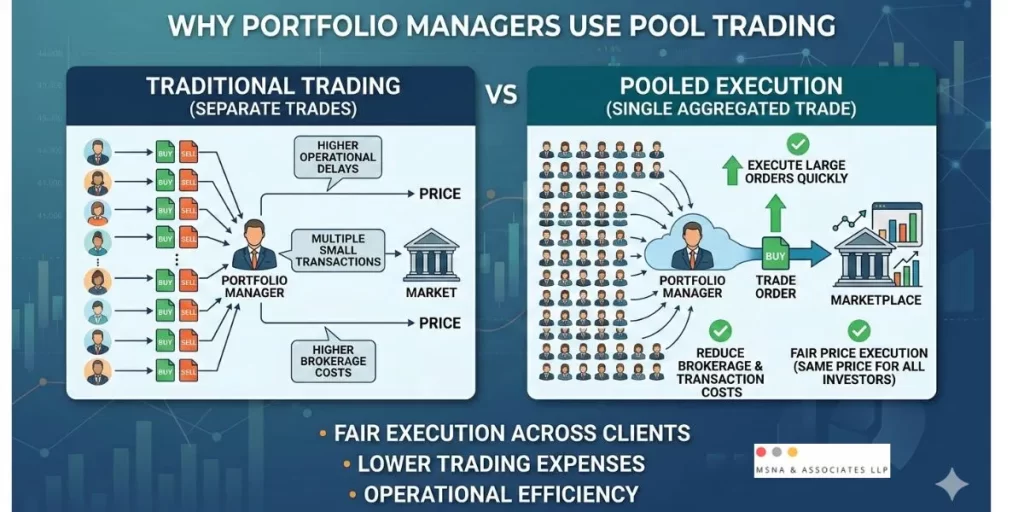

Why Portfolio Managers Use Pool Trading in PMS?

Portfolio managers adopt pool trading primarily for operational efficiency and fair execution.

In a PMS structure, hundreds of client portfolios may hold similar investment strategies. If a portfolio manager placed separate trades for each client account, it would create significant operational delays and higher brokerage costs.

Instead, pooled execution allows managers to:

Execute large orders quickly in the market

Reduce brokerage and transaction costs

Ensure all investors receive the same execution price

Maintain consistent portfolio allocation across clients

For example, if a PMS strategy requires purchasing 10,000 shares of a stock across 50 clients, the portfolio manager executes one aggregated order and later distributes the shares across client portfolios according to allocation rules.

This approach ensures fair pricing and operational scalability, especially for large PMS strategies managing hundreds of crores in assets.

Regulatory Framework Governing PMS Pool Trading in India

The PMS pool trading process operates under strict regulatory supervision.

Under Regulation 24(12) of the SEBI PMS regulations:

Portfolio managers must normally execute trades separately for each client.

However, they may aggregate orders to achieve economies of scale.

When aggregation occurs, they must allocate trades pro-rata at the weighted average price.

Allocation must occur within the same trading day.

The portfolio manager cannot keep any unallocated open position.

These regulations prevent unfair trade allocation and ensure that portfolio managers do not favor specific clients.

Such safeguards are critical because PMS accounts often manage significant capital from high-net-worth investors and institutions.

Why NRI Investments Cannot Be Pooled in PMS Structures?

While pooling works for resident investors, Non-Resident Indian (NRI) investments follow stricter compliance requirements.

Under guidelines issued by the Reserve Bank of India and regulations under the Foreign Exchange Management Act (FEMA), NRI investments must maintain clear traceability.

Pooling NRI funds could create regulatory challenges, such as:

Difficulty in monitoring repatriation rules

challenges in identifying investor-specific transactions

complications in regulatory reporting

Therefore, PMS providers maintain separate operational structures for NRI investments, ensuring compliance with FEMA reporting requirements.

Key Participants in the PMS Pool Trading Process in India

Several regulated institutions participate in the PMS trade lifecycle. Each participant performs a specific role to ensure smooth trade execution and settlement.

Portfolio Manager

The portfolio manager drives all investment decisions. They generate trade sheets based on the PMS strategy and the client’s existing portfolio holdings.

They also ensure that the final allocation complies with regulatory rules.

Broker

The broker acts as an intermediary between the PMS and the stock exchange. Brokers execute buy and sell orders on behalf of the PMS.

Stock Exchanges

Trades are executed on regulated stock exchanges such as the National Stock Exchange of India and BSE Limited.

These exchanges provide transparent trading systems and ensure fair price discovery.

Clearing Corporations

Clearing corporations handle post-trade settlement and guarantee the completion of transactions.

They ensure that buyers receive securities and sellers receive funds.

Custodian

A custodian safeguards client securities and cash. Under SEBI rules, PMS providers must appoint a custodian registered under the SEBI (Custodian of Securities) Regulations, 1996.

The custodian performs several critical functions:

settlement verification

trade confirmation

client-wise allocation

asset safeguarding

This independent oversight strengthens investor protection.

Depositories

Depositories maintain securities in electronic form.

India currently operates two primary depositories:

National Securities Depository Limited

Central Depository Services Limited

Depositories ensure accurate ownership records for investors.

Step-by-Step PMS Pool Trading Workflow

The PMS pool trading process in India follows a structured workflow that connects portfolio management decisions with final settlement.

Step 1: Trade Sheet Generation

Before the market opens, the portfolio manager compares the model portfolio with the existing client portfolios.

Based on the required adjustments, the manager prepares a trade sheet containing all securities that need to be bought or sold.

This trade sheet aggregates orders across multiple client portfolios.

Step 2: Trade Execution on Stock Exchanges

The portfolio manager forwards the trade sheet to the broker.

The broker executes the orders on the exchange trading platform. Once buy and sell orders match, the exchange confirms trade execution.

However, securities do not transfer immediately during this stage.

Step 3: Clearing and Settlement

After trade execution, transactions move to the clearing corporation.

The clearing corporation coordinates:

transfer of securities from sellers

transfer of funds from buyers

Upon successful settlement, purchased securities move into the PMS Pool Demat Account controlled by the custodian.

Step 4: Client-Wise Trade Allocation

After market closure, the broker sends a trade confirmation report to the PMS.

The PMS system generates a Trade Allocation File specifying:

client allocations

trade quantities

weighted average price

The custodian uses this file to allocate securities to each client’s Demat account.

Step 5: Settlement of Sale Transactions

For sale transactions, the settlement process operates in reverse.

The custodian earmarks securities from client Demat accounts and transfers them to the clearing corporation on the settlement date.

Once the settlement completes:

buyers receive the securities

Sale proceeds move to the PMS pool bank account

Portfolio managers can then redeploy these funds for future investments.

SEBI regulations require PMS providers to clear the pool demat account by the end of the trading day, ensuring no residual positions remain unallocated.

How PMS Pool Trading Improves Market Efficiency?

The PMS pool trading framework enhances the efficiency of portfolio management operations in several ways.

First, it allows portfolio managers to execute large orders efficiently without placing multiple individual trades.

Second, it ensures uniform pricing across investors, since all allocations use the same weighted average price.

Third, the involvement of custodians and clearing corporations strengthens regulatory oversight and operational integrity.

Finally, SEBI’s allocation rules protect investors from potential conflicts of interest in trade allocation.

As PMS assets under management in India continue to grow, such structured processes become increasingly important for maintaining transparency and trust in professional portfolio management.

Conclusion Related To PMS Pool Trading Process In India

The PMS pool trading process in India ensures that portfolio managers can execute trades efficiently while maintaining fairness and regulatory compliance.

Through a coordinated system involving brokers, custodians, clearing corporations, and depositories, trades move through a clearly defined pipeline from trade sheet generation to final settlement in client Demat accounts.

For investors, understanding this process helps build confidence in how professional portfolio managers operate within India’s regulated capital markets ecosystem.

Need clarity on investment structures, PMS operations, or regulatory frameworks?

Related

Discover more from MSNA & Associates LLP

Subscribe to get the latest posts sent to your email.